Rates as of 05:00 GMT

Market Recap

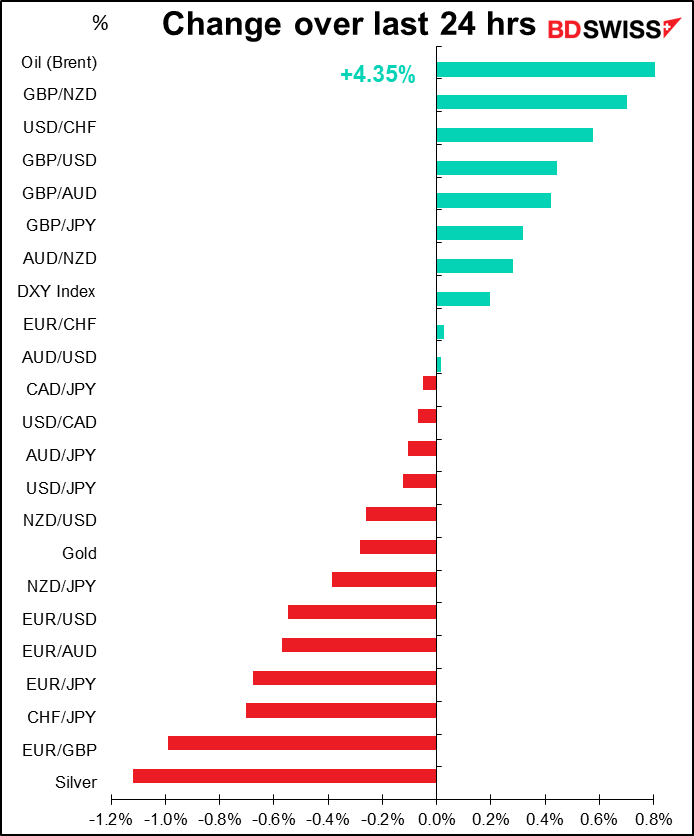

Well, it’s bye-bye Boris! I had expected that his departure would cause some near-term uncertainty and thereby cause the pound to weaken, although in the longer term his departure would probably be seen as a Good Thing and cause GBP to strengthen – not least because perhaps the next person will be able to do a better job in negotiating with the EU over Northern Ireland. Looking at the cross rates below, the FX market apparently skipped the first part and went right to the second part.

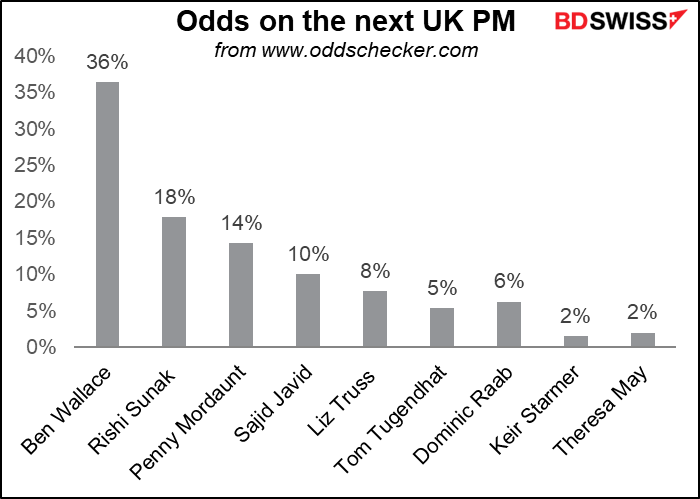

Who’s going to be the next PM? According to the site oddschecker.com, which aggregates the odds from various betting sites in the UK, Ben Wallace is the clear frontrunner.

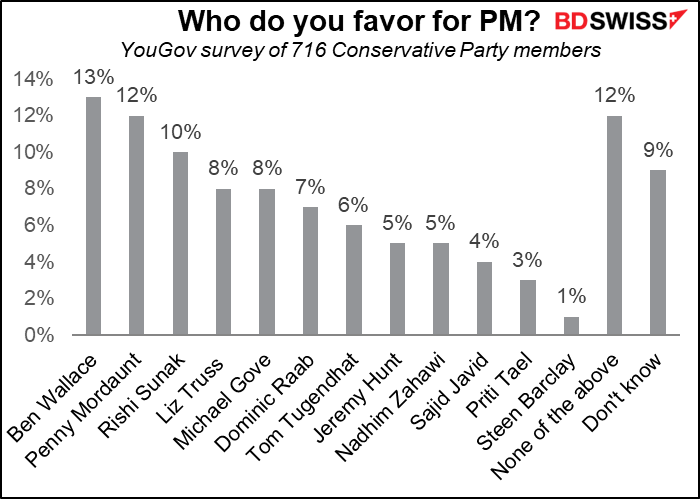

A YouGov survey of 716 Conservative Party members turned up the same front-runner. And although Wallace has only a modest lead in this poll, when placed in a one-to-one choice against the others, he clearly dominates. For example, 48% of the people polled favored him vs Penny Mordaunt, the #2 candidate in this poll, vs only 26% who favored her. Similarly, 51% favored Wallace over Sunak, the #2 in the betting odds, vs only 30% who favored Sunak.

Mr. Wallace is a former soldier currently serving as Secretary of State for Defence. He declined to say if he’d run, insisting that he was just going to concentrate on doing his job. (hahaha)

Although Wallace was an early supporter of Johnson, there’s one big difference between them: Wallace supported “Remain” in the Brexit referendum, although he later voted in favor of PM May’s Brexit withdrawal agreement and voted against any referendum on a Brexit withdrawal agreement. His pro-Remain stance could mean a more conciliatory posture toward the EU in the current negotiations over Northern Ireland, which reduces the chances of a trade war and is therefore positive for the UK economy and for sterling – although of course I’m forecasting his future policy on a stance he took in 2016, so it’s by no means certain.

While there is some question about the Bank of England’s room for maneuver when UK politics are in flux, comments from Monetary Policy Committee (MPC) members yesterday didn’t show any reluctance to pause the tightening cycle while politicians get their act together. External MPC member Catherine Mann said GBP is an important metric for the central bank and “in the near term, tighter US monetary policy tends to boost UK inflation because of the weaker currency” and “a robust policy response to avoid near-term augmentation of inflation dynamics is appropriate in today’s environment.” Mann was one of the three MPC members who dissented at the last meeting, preferring to hike by 50 bps rather than 25. Her comments were echoed by BoE Chief Economist Pill, who said the BoE is “willing to move faster on rates if needed.”

To make matters worse, yesterday’s Decision Maker Panel survey showed inflation expectations rising further – meaning that the Bank will have to act more aggressively to rein in expectations.

Meanwhile, the best trolling I saw was from the Blackpool branch of the wax museum Madame Tussaud’s. They took their statue of Boris and put it outside the local Job Centre (where unemployed people go to look for work).

Even the Americans got in the act! Four Seasons Total Landscaping, that famous place where Rudi Guiliani held a press conference (mistaking it for the upmarket Four Seasons Hotel, presumably) sent out this tweet:

And of course the spoof UK news reporter Jonathan Pie had some choice words to say on the subject, most of which were obscene & vulgar. Don’t watch if you’re easily offended. Or even just a little difficult to offend.

At the other end of the emotional spectrum, I was shocked and saddened to read of the shooting of former Japan PM Shinzo Abe. While I disagreed with a lot of his politics, he certainly did not deserve this.

JPY gained (USD/JPY fell) in response to the shooting, for two reasons: one, the Tokyo stock market fell after the shooting (although it remained in plus territory for the day) and JPY usually gains in any “risk-off” environment.

Secondly, Abe was a strong proponent of monetary easing, which was one of the “three arrows” with which he hoped to revive the Japanese economy. He was also the person who appointed Bank of Japan Gov. Kuroda. For some reason some market participants fear that his absence could weaken support for easing, although I disagree. It’s true that in Japan, some politicians retain a lot of influence even out of office (in a similar manner to the way retired emperors used to rule from behind the throne, the “insei” or cloistered government system of the 11th and 12th centuries). However that ignores the fact that PM Kishida, the current PM, is also a strong proponent of monetary easing and Gov. Kuroda will be in office until next April. Indeed there don’t seem to be many people in Japanese politics arguing for a tightening of monetary policy, so I doubt if Abe’s departure would change anything.

Elsewhere, EUR continued to weaken (EUR/USD declined) even though the minutes of the June meeting of the European Central Bank (ECB) June described a 25 bp hike in July as a “proportionate first step,” and note that a “larger increment” would be appropriate in September if the medium-term inflation outlook hadn’t improved by then – as looks quite probable. The problem plaguing the currency seems to be recession fears as European gas prices rose further. German gas prices rose 7.8% and Dutch prices 6.8%, the seventh consecutive day of rising gas prices. Higher gas prices of course fan inflation fears too, but recession seems to trump inflation.

Elsewhere, prices of most commodities – and the commodity currencies – rose as China announced some $220bn in fiscal stimulus by pulling forward infrastructure investment in the second half of the year.

Today’s market

Note: The table above is updated before publication with the latest consensus forecasts. However, the text & charts are prepared ahead of time. Therefore there can be discrepancies between the forecasts given in the table above and in the text & charts.

There’s a three-day conference that starts today, the REAix2022 conference, “Successfully Transforming the World,” taking place in Aix-En-Provence, France, and online. A number of important speakers will be talking in the 61 sessions. ECB President Lagarde kicks off today with a panel discussion on “What is the world at risk of?” You can submit a question if you like!

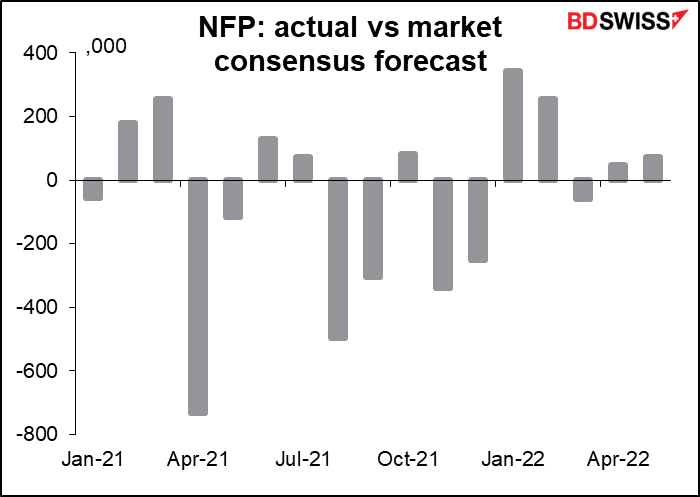

Then it’s on to the main event of the day, the ever-loving US nonfarm payrolls (NFP). I discussed this in some detail in my Weekly Outlook, as always, but since I get paid by the word I’ll repeat what I said there and use the extra money to buy my lunch today. See you at Columbia Beach!

The market consensus forecast for payrolls is +268k, which would be the smallest increase since +200k in Dec. 2019 (there have been several months when payrolls fell however). This is still a healthy level but a slowdown nonetheless – the six-month moving average is 505k a month. Looking at the graph, it’s clear that hiring has slowed over the last four months.

The slowdown isn’t due to any shortage of jobs. The Job Offers and Labor Turnover Survey (JOLTS) for May, out earlier this week, showed that there were still 11.3mn job openings in May, meaning 1.89 jobs for every unemployed person – not far off the record high of 1.99.

The unemployment rate is expected to stay at 3.6% for the fourth month in a row, near the 50-year low of 3.5% achieved right before the pandemic hit. The participation rate is forecast to creep up another one tick. All good stuff!

The reason people watch the NFP so closely is that the US Fed has a “dual mandate” – it’s required to pursue “the goals of maximum employment, stable prices, and moderate long-term interest rates.” Employment is therefore a limiting factor for the Fed – if the US economy gets too far away from “maximum employment” they’ll have to decide between supporting employment (a looser policy) or fighting inflation (a tighter policy).. However with the US unemployment rate at 3.6% and nearly 2 jobs available for every unemployed person, I don’t think anyone believes employment is limiting what actions the Fed can take now.

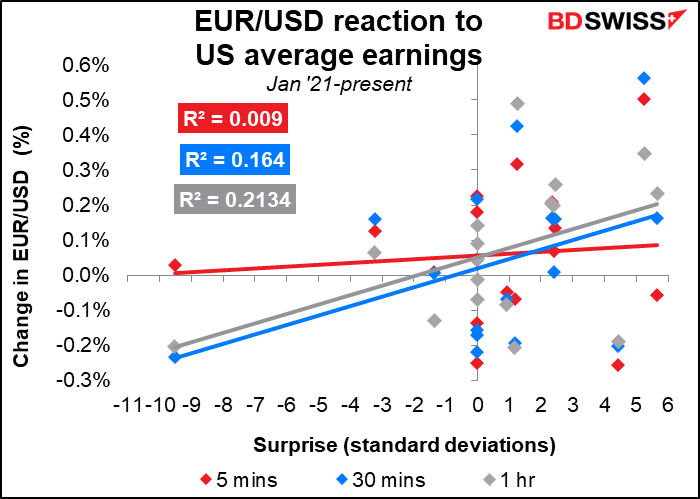

Instead, the Fed is focused on the inflation aspect of its dual mandate. For that reason I think the average hourly earnings (AHE) are likely to be more significant for the market than the NFP figure itself. If companies have to pay higher wages, they’ll eventually have to raise their prices to compensate. The result would be a wage-price spiral that keeps inflation rising intractably.

Looking at the forecast for this month’s average hourly earnings, there doesn’t seem to be much risk of a wage-price spiral at present. Wages are expected to be up 5.0% yoy, well below the 8.6% yoy rate of inflation. Furthermore, the rate of growth in wages slowed in April and May and is expected to slow further in June. So don’t worry, workers are losing out and your dividends are safe. The slowing trend in wages should alleviate some concern that the Fed will have to tighten drastically to get inflation down. That could be negative for the dollar.

How do the forecasters do? Economists’ track record for forecasting the NFP is pretty much as you’d expect: a coin toss. Since Jan. 2021 the NFP has beaten forecasts 9 times and missed forecasts 8 times. Or looked at properly, economists have underestimated the NFP 9 times and overestimated 8 times.

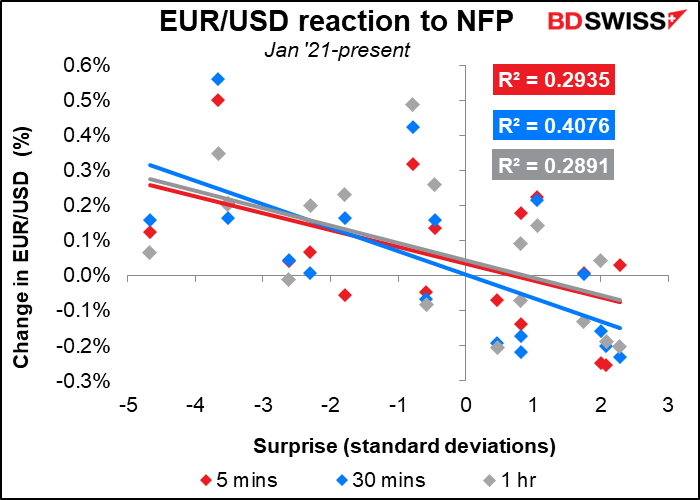

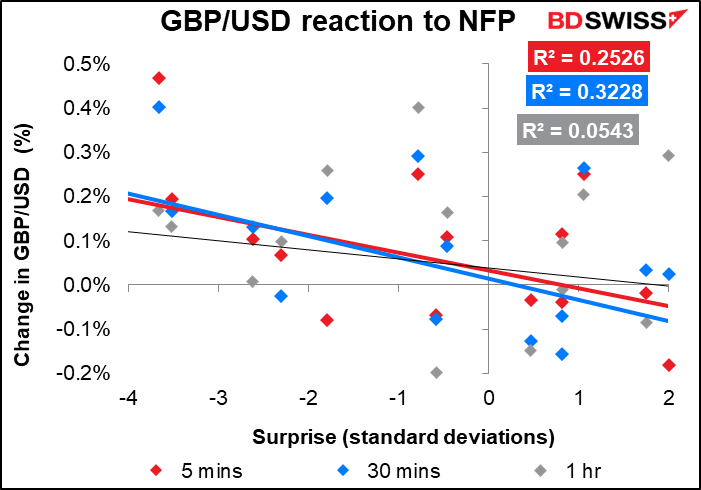

Likely market reaction: Currencies do react quickly and strongly to the NFP headline number.

The reaction to the unemployment rate isn’t that strong

Nor is the reaction to the average hourly earnings, at least not initially. It is noticeable though that the correlation between the surprise in average hourly earnings and the change in the currency increases over time, rather than decreasing as happens with most indicators. It may well be that traders immediately react to the headline NFP number, then as they get a chance to look at the other figures, they start to consider the inflationary impact of the earnings figure. Also it takes some time for Wall Street economists to crunch the numbers and disseminate their views to the sales force and the clients. The increasing correlation could also be a function of that delay.

Longer-term reaction: Looking at the last six times the NFP beat estimates and the last six times it missed, it seems that the results didn’t matter: on average, the dollar strengthened in the following days no matter what happened. Of course the average masks some times when it gained and some times when it lost, but that’s the odd result. My interpretation is that while the figure may have been above or below market estimates, it was always judged to be enough to keep the Fed on a tightening path and therefore positive for the dollar. I’m not sure the same way of thinking is likely to hold sway still however because, as I said above, full employment is already in everyone’s playbook and therefore not necessarily sufficient to sway anyone’s views on the dollar.

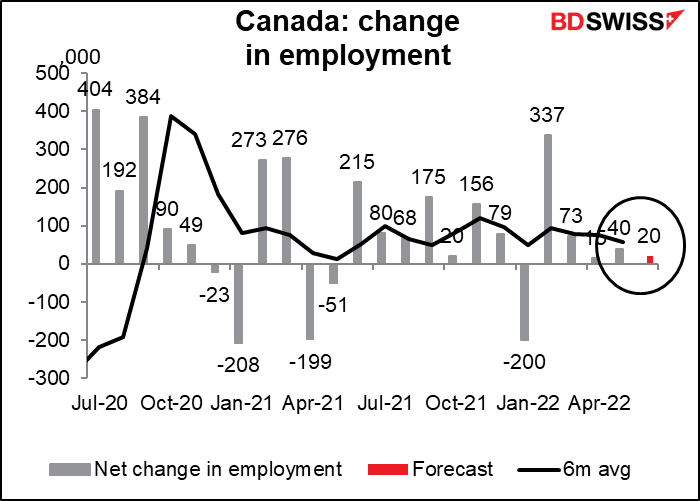

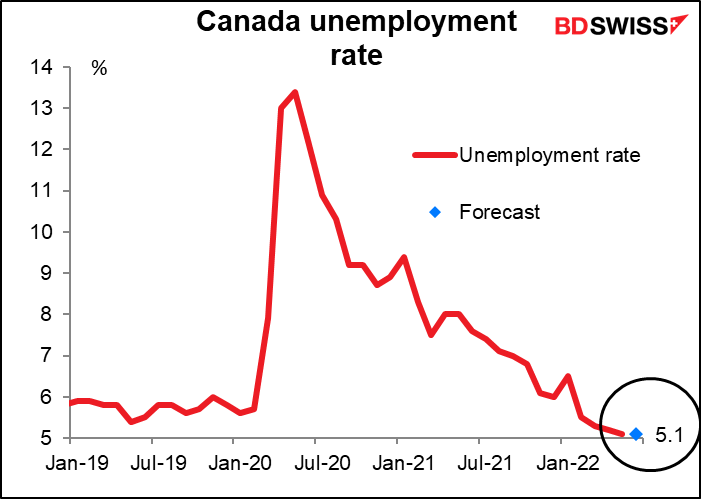

Lest we forget, Canada also announces its employment data at the same time as the US. The rise in employment has been slowing for some time. It’s expected to be up a mere 20k this month, vs the 6-month average of 57k.

Like in the US, that may be due more to there being few people left who want to work but can’t find a job. The unemployment rate is expected to be unchanged at 5.1%. “Unchanged” in this case is pretty good as 5.1% is the record-low rate (data back to 1976). I think unemployment continuing at the record-low rate would be positive for CAD.

Which of these two indicators should you watch if you’re trading USD/CAD? Both. Both have a high correlation with the subsequent movement of USD/CAD. The unemployment rate has a higher Bloomberg relevance score but the change in employment has a slightly higher correlation with the subsequent movement in the currency (although I’m not sure that the difference between the two is statistically significant).

On Sunday, Japan goes to the polls for the Upper House election. The only question in this election is how big a majority the ruling Liberal Democratic Party (LDP), which is neither liberal nor democratic, and its ally the Komeito, are likely to win. Support for the Kishida administration remains solid and some polls have suggested the LDP/Komeito alliance could increase its pre-election majority in the Upper House. That would give the administration a huge boost in political capital and enable PM Kishida to pursue his own policy priorities up until the next election, whenever that might be.

Of particular interest will be his decision on a successor to Bank of Japan Gov. Kuroda, whose term of office is up in April next year. The selection process will get underway shortly after the election. The larger the LDP’s majority, the greater the chances of a change in the government’s monetary policy stance. Given the strong support PM Kishida has shown so far for Gov. Kuroda’s stubbornly stimulative policy, I doubt he would suddenly change to a more hawkish stance. More likely he’d consider appointing someone even more aggressive about a loose monetary policy, like BoJ Board Member Goushi Kataoka, who dissents at every meeting because he believes “further coordination of fiscal and monetary policy” is necessary and he wants “to further strengthen monetary easing by lowering short- and long-term interest rates.” That would be negative for the yen. However I doubt if the market will make an immediate connection between Sunday’s election and the eventual appointment of a new Governor next April, so the election is not likley to be a major factor for the FX market.