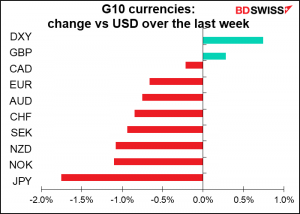

We heard from three central banks this week: the Reserve Bank of New Zealand (RBNZ), the Bank of Canada (BoC), and the European Central Bank (ECB). The first two hiked by 50 bps, the latter of course kept rates steady. All three warned of the same thing: the risk that people begin to think that the current high level of inflation will last for a long time. They said as follows:

RBNZ: The Committee will remain focused on ensuring that current high consumer price inflation does not become embedded into longer-term inflation expectations.

BoC: There is an increasing risk that expectations of elevated inflation could become entrenched. The Bank will use its monetary policy tools to return inflation to target and keep inflation expectations well-anchored.

ECB: While various measures of longer-term inflation expectations derived from financial markets and from expert surveys largely stand at around two per cent, initial signs of above-target revisions in those measures warrant close monitoring.

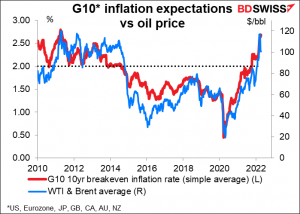

It is true. Inflation expectations in the three currency zones are indeed rising.

Why are they so worried about this? Because economists believe that if people start to think that inflation is going to be higher in the future, they’re going to demand higher wages to make up for it. Then companies will raise their prices to cover the higher wage costs and the fears will become true – prices will rise faster. Which will just encourage people to demand a bigger hike in wages at the next negotiating round. In other words, the fear is that rising inflation expectations can set off a wage/price spiral that makes it hard to tame inflation. Furthermore, economists worry that if companies expect inflation to remain high they are likely to keep raising their prices so that they can cover the cost of replacing their inventory, or even just take advantage of generally rising prices to raise their prices too (“me-too” price hikes).

The question is, is there any basis in fact for these theories? Some economists say no. A recent paper by an economist working for the Board of Governors of the Federal Reserve (“Why Do We Think That Inflation Expectations Matter for Inflation? (And Should We?)”) argued that “history really only tells us that lags of actual inflation seem to enter inflation equations to a greater or lesser degree over time, not that expectations do or did; thinking that these lags of inflation are present because they are a proxy for some kind of forecast is more a habit of mind than anything solidly grounded in fact.” He concludes, “…we have nothing better than circumstantial evidence for a relationship between long-run expected inflation and inflation’s long-run trend, and no evidence at all about what might be required to keep that trend fixed…”

A recent paper prepared for the European Parliament’s Committee on Economic and Monetary Affairs (ECON committee) (Should rising inflation expectations concern the ECB?) agreed. It argued that “There is limited evidence of survey measures of inflation being useful for forecasting inflation.” “The traditional wage-bargaining mechanism through which expected inflation should raise inflation is likely to be weak in a world with low levels of unionization,” it said. It also noted that “Central bank efforts to influence the public’s inflation expectations may be limited in usefulness. Most people pay no attention to central banks and many have poorly informed opinions on inflation.”

A similar conclusion from another paper in that series (What to expect from inflation expectations: theory, empirics and policy issues). “The overall picture of theoretical and empirical studies is more shadowed than usually believed,” it said. “Granted that information on future inflation expectations has to be carefully assessed and processed along with other information… caution suggests it should not be given the role of polar star of monetary policy.”

In short, central banks seem to be placing a lot of importance on something that may not actually be particularly important. Given the leads and lags in forming inflation expectations and the stickiness of people’s views once they’re established, this could lead central banks to make a policy mistake on the upside and plunge economies into a recession to stamp out something that doesn’t matter.

In any case, inflation expectations seem to me to be largely a function of oil prices so I’m wondering what the big deal is anyway.

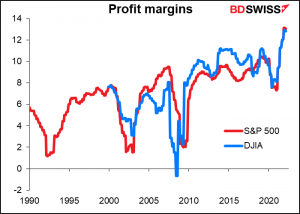

One thing that may be helping to push up inflation currently is not high wage settlements as the “inflation expectations” theory would predict but rather corporate greed. If we look at the companies in the S&P 500 and Dow Jones Industrial Average, their profits margins are the highest in at least 32 years. (I don’t have data before that.)

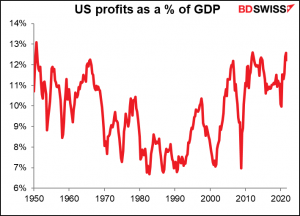

If we look at profits as a percent of GDP, in Q3 last year they tied the Q1 2012 record of 12.6%, which has only been beaten once – in Q4 1950 (13.1%). So I would guess that corporate greed is a bigger factor in the current high level of inflation than rising inflation expectations spurring wage/price spirals. I eagerly await Bank of England Gov. Bailey’s admonishments to companies to “show restraint” in their profits just as he has urged workers to “show restraint” in their wage settlements to avoid upward pressure on inflation. (I have to admit I don’t have the same data for the UK so I’m not sure it applies to the country.)

.

Next week: more inflation data, preliminary PMIs, IMF/World Bank Spring meeting

The week gets off to a slow start as Monday is a holiday (Easter Monday) in Australia, New Zealand and most of Western Europe, though not the US.

For those of you who are wondering about inflation, which probably is everyone who is thinking about economics nowadays, there’s going to be plenty of data worth watching next week. We get consumer price indices (CPIs) from Canada (Wednesday) New Zealand (Thursday), and Japan (Friday), plus German producer prices on Wednesday and the final CPI for March for the EU on Thursday.

Will anyone be surprised if the general trend is for inflation to rise in these countries?

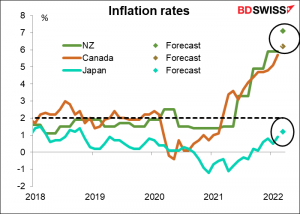

New Zealand: as NZ has only quarterly inflation data, it’s even more important than elsewhere. Headline inflation is expected to leap to 7.1% yoy vs 5.9%

Canada: headline CPI is forecast to rise to 6.2% yoy from 5.7%. Another month of 1% mom inflation. Ouch!

Japan: Even Japan, the perennial outlier, is forecast to see rising inflation. Headline inflation is forecast to rise 1.2% yoy, the first time over 1% since October 2018. However core inflation (excluding fresh food & energy) is forecast to remain in deflation of -0.8% yoy. We’re all just waiting until next month, when the plunge in mobile phone charges a year ago drops out of the calculation, to see what happens then. Headline inflation will probably go over 2%. How will the Bank of Japan react to that? Tune in on May 19th to find out!

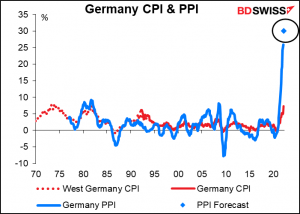

Meanwhile, the German producer price index (PPI) is forecast to rise at the astonishing rate of 30% yoy. Ach du Lieber Güte! OK much of this is due to energy but still…The gnomes at the Bundesbank must be nearly apoplectic.

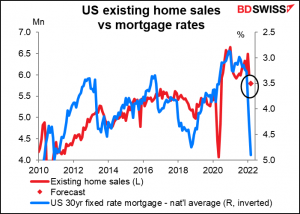

For the US, the other main indicators will be housing statistics, namely housing starts (Tue) and existing home sales (Wed). It’ll be interesting to see how the rise in mortgage rates has affected the housing market. If history is any guide, housing should be cooling off as mortgage rates rise to the highest level in a decade. This is after all one major way in which Fed tightening acts to cool inflation, namely by cooling demand.

For the US, the other main indicators will be housing statistics, namely housing starts (Tue) and existing home sales (Wed). It’ll be interesting to see how the rise in mortgage rates has affected the housing market. If history is any guide, housing should be cooling off as mortgage rates rise to the highest level in a decade. This is after all one major way in which Fed tightening acts to cool inflation, namely by cooling demand.

More importantly perhaps Parliament comes back into session and there will be all sorts of comments about PM Boorish Johnson and Chancellor Rishi “My Wife Doesn’t Live Here” Sunak being fined for partying during the lockdown period. Johnson now has the dubious honor of being the first sitting PM to be sanctioned for breaking the law.

So far 70 Conservative Party MPs and most of the cabinet have slavishly defended him while only one Conservative Party MP has called on Johnson to resign. The prime minister can only be removed by a vote of no confidence in Parliament or by his own MPs organizing a leadership contest, neither of which is likely to happen right now, because who wants to stand for re-election if they can avoid it? So this will probably blow over even if, as seems likely, he gets fined for three more events. Look what happened with Trump being impeached twice – it took an election to dislodge him.

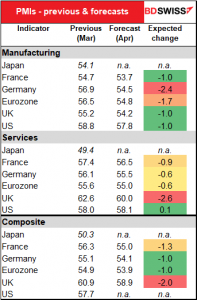

Friday also sees the preliminary purchasing managers’ indices (PMIs) for the major industrial countries. They’re expected to be lower across the board. The only one that’s forecast to be higher is the US service-sector PMI, and even that’s forecast to be up just a measly 0.1 point.

I’m puzzled as to why the service sector is expected to see such declines. Most of the countries in question have been loosening up their restrictions and so one might imagine more people going to restaurants, movies, gyms, etc.

Finally, Tuesday through Saturday will be the Spring Meeting of the IMF and World Bank. You can watch a lot of the meetings & events live on their website. The big event will be at 17:00 GMT Friday, when Fed Chair Powell, ECB President Lagarde, and three other people you’ve probably never heard of debate The Global Economy. Alongside the IMF/World Bank meetings, the Peterson Institute for International Economics (PIIE) has organized “Macro Week 2022.” This string of events will feature Swiss National Bank Chairman Thomas Jordan (Tue), Bank of England Gov. Bailey (Thu), and ECB President Lagarde (Fri). All events will be webcast live on the page I linked to. Be there or be square!

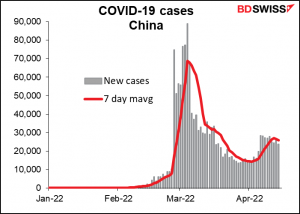

Other points to watch out for next week are the COVID-19 situation in China, which is seeing a rise in cases again after it looked like they were getting under control. This could have a major impact on global supply chains as truckers and shipyard workers are forced to stay home, thus disrupting global trade.

Finally, stock markets will be looking out for earnings from several bellwether US companies, such as American Express, Netflix, Tesla, and Procter & Gamble.