Rates as of 04:00 GMT

Market Recap

I have to admit, I’m confused by the market’s response to the Fed statement. On the one hand, it was pretty much in line with expectations – rates on hold at least through 2023 and no change in the rate or maturity of Treasury purchases, as expected. The only modest surprise was that they rewrote the forward guidance language to be more consistent with the new policy framework, but since everyone knew the new policy framework, that didn’t hold any surprises.

What came through in the press conference though is that the formal statement doesn’t tell the whole story. First off, I think the Fed has switched from targeting inflation to targeting unemployment. They’ve always had this dual mandate, but previously it seemed that the employment part was subordinate to the inflation part – that they worried about unemployment being too low because of its possible impact on inflation (that is, inflation was the concern and they looked at the employment situation as one factor that could influence inflation). Now they seem to be much less worried about inflation and more concerned about unemployment – specifically, unemployment being too high, not too low.

My suspicion is that this change in emphasis stems from the “Fed Listens” program, when Fed officials went around the country listening to average citizens talking about how Fed policy impacts their lives. During this road show they heard a lot about the benefits that lower unemployment brought to people at the bottom of the wage scale. This has brought about a big change in their thinking about just what the aim of monetary policy should be.

“We view maximum employment as a broad-based and inclusive goal, and did not see a high level of employment as posing a policy concern unless accompanied by signs of unwanted increases in inflation or the emergence of other risks that could impede the attainment of our goals,” Powell said. “…when we think about maximum employment in particular, we do look at individual groups. So the high unemployment in a particular racial group, like African Americans, we would look at that as we think about whether we’re really at maximum employment.”

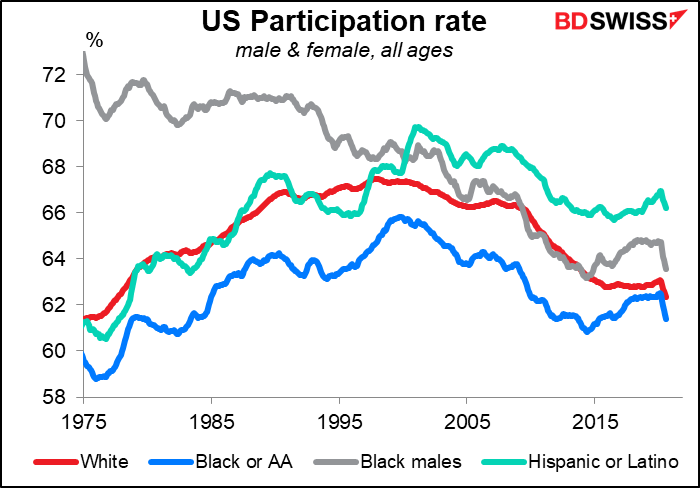

One huge change in the US employment situation over the years has been the stunning decline in the participation rate for Black males. It finally started to rise over the last five years, which brought great benefits to marginalized communities.

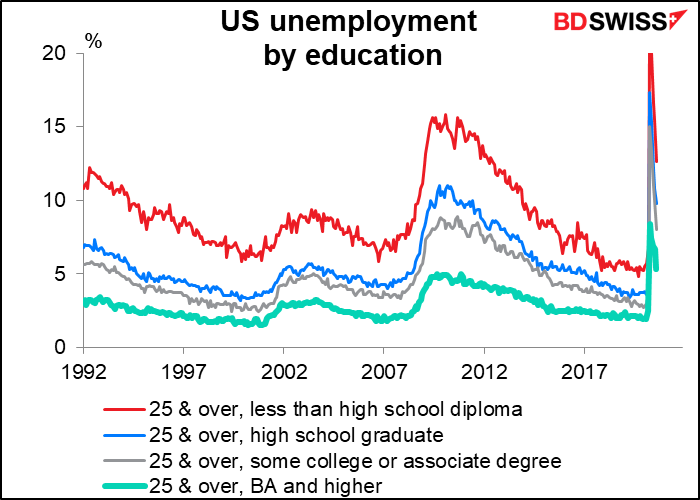

But as Powell repeatedly emphasized, the pandemic has hit low-wage workers in the service sector much harder than higher-waged people in knowledge-based industries. Unemployment has always been higher for people with less education, but they really got a knock in this downturn. I think that unless inflation is clearly over 2% and accelerating, they are likely to keep rates low indefinitely to allow these groups to improve their employment situation.

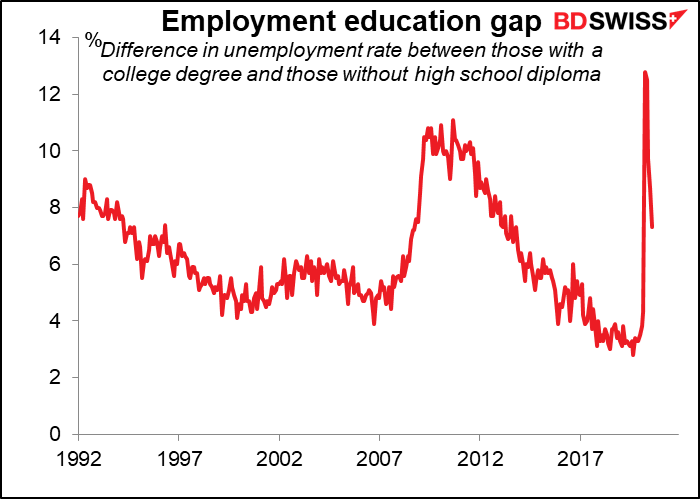

(N.B. – I think the “employment education gap” graph explains a lot about the popularity of Trump, too. Although the rate began falling well before he got elected, it does explain a lot why people without a college education would vote for a total outsider who promised to come to Washington and shake things up.)

One other point: I don’t include a graph of the “dot plot” this time because it’s so simple. Everyone agrees that the fed funds rate will stay at zero next year. One person thinks it’ll rise to 0.625% in 2022, but the other 16 think it’ll be unchanged. In 2023, 13 of the 17 people – an overwhelming majority – think it’ll still be at zero, while two people expect one rate hike (and two expect more).

The hidden question is: what about 2024? Powell was asked about that in the press conference, because the Summary of Economic Projections (SEP) gives the Committee’s median forecast of inflation (both headline and core) for 2023 as 2.0%, yet the Fed has pledged to keep rates unchanged until inflation is above 2.0%. Powell was asked, since the SEP doesn’t show the Fed hitting its target of above-2% inflation, how confident are they that they will eventually hit the target? He responded that “the projections don’t show the out years.” IE, we must assume that they think they’ll hit the target in 2024. But that doesn’t mean they will raise rates in 2024 – they’ve pledged to allow inflation to run above 2% so that it averages 2% over time. In other words, while the dot plot has them keeping rates at zero until 2023, the odds are that if their forecasts are correct, they will keep rates at zero in 2024 as well. I think that should be more negative for the dollar and positive for gold than it was.

Other points: Powell also made it clear that the Fed’s forecasts depended on more fiscal stimulus being available, and the failure to come up with another fiscal package would involve “downside risks,” as he said diplomatically. He also mentioned three times that people should wear masks, in comments such as “Following the advice of public health professionals to keep appropriate social distances and to wear masks in public, will help get the economy back to full strength.”

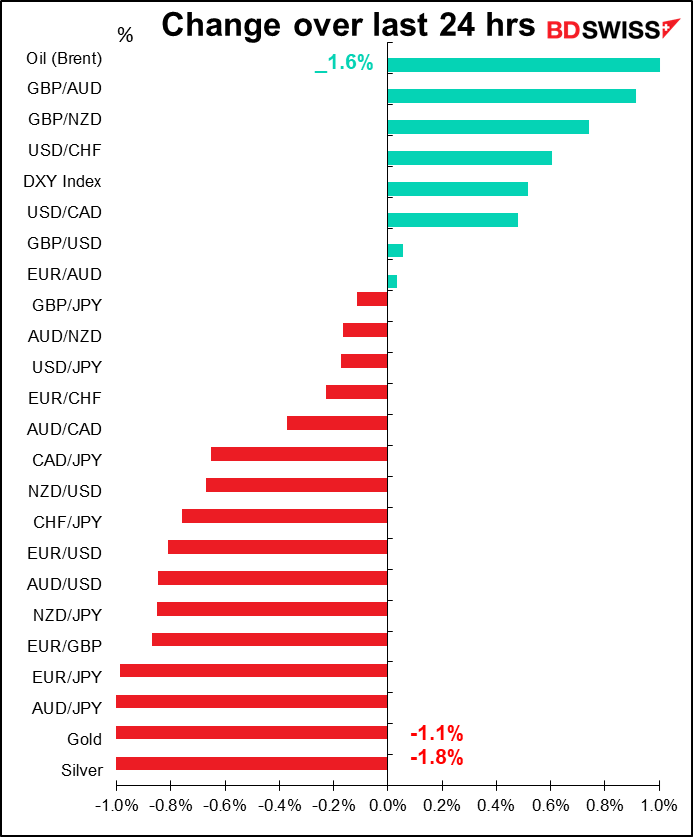

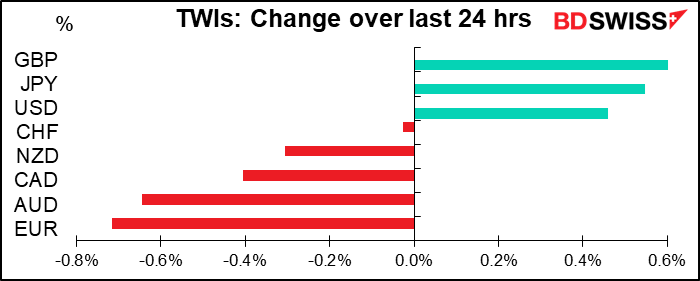

Elsewhere in the market, GBP continued to recover. This seems to be short-covering after the big drop over the last few days. Although core inflation hit a five-year low just outside the Bank of England’s target range (0.9%), it wasn’t as low as expected (0.5%) and buyers came in afterward.

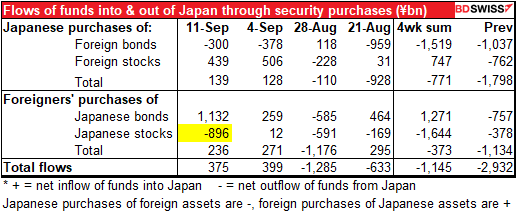

The really puzzling thing to me is why the yen continues to appreciate. Most of the rise takes place during London and New York trading, not Japan time, which implies that it’s foreign investors doing the buying. Can it be that they are optimistic about the new Suga administration, or that they’ve been encouraged by Warren Buffet’s newfound enthusiasm for Japanese stocks? The latest data say no, that foreigners remain net sellers of Japanese stocks, although we’ll have to see what next week’s data says.

Maybe it’s the narrowing of the interest rate differential with the US. That is, everyone knew Japanese short rates would be unchanged at around zero until the end of the Holocene epoch, but now that it looks like US rates will be unchanged until the end of the Subatlantic chronozone, there’s less reason to use JPY exclusively as a funding currency.

I wonder too if this is related to the fall in EUR. EUR/JPY has been particularly weak as investors have been cutting their positions, particularly through options. The 124.50 line has provided support several times in the last two months, with 124.38 the recent low (Aug 10). Breaking through that support has apparently sent it lower, which may be spilling out into EUR/USD as well. Other than that, ECB Executive Board member Schnabel reiterated in an interview that the ECB was monitoring (as opposed to targeting) exchange rate movements — the same point that other Board members have stressed,

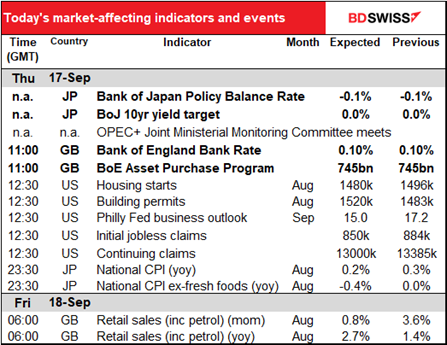

Speaking of Japan, the Bank of Japan met overnight as well. It went quite as expected – no change in their policy and a bit more optimistic about the economy, saying that the economy had started to pick up with activity resuming gradually.

Today’s market

The big excitement today is the Bank of England Monetary Policy Committee (MPC) meeting. With the Bank of England (BoE), it’s more a matter of “when,” not “whether” or “what.” The market is pricing in a Bank Rate of -0.10% by next June, vs a target rate of +0.10% today. Most of the recent comments by BoE officials have been to reassure the markets that “we are not out of firepower by any means,” as BoE Gov. Bailey said at the Jackson Hole virtual symposium.

That doesn’t mean anything specific for this meeting, however. With no update on the forecasts, no press conference scheduled, with Brexit talks looking like the parrot sketch from Monty Python (the UK position is that the Withdrawal Agreement is “just resting”), I can’t imagine that the Bank would take any decisions at this time. Furthermore, with July GDP up 6.6% mom and industrial production gaining, they may be getting a bit more optimistic about the economy – the UK has recovered about half the lost level of output.

One concern — the fall in inflation for August, announced yesterday — might give them pause. Yesterday’s inflation figures are just enough to trigger a letter from the Governor to the Chancellor explaining what the Bank is going to do to get inflation back within its acceptable range. I suspect they say some variation on “we are not out of firepower by any means,” as BoE Gov. Bailey said at the Jackson Hole virtual symposium.

I expect another unanimous decision to keep policy unchanged and an update on how the economy is going relative to the optimistic projections set out in the August Monetary Policy Report (MPR). Other than that, not much. The excitement is likely to come in November, when the Brexit endgame is known and the next MPR brings revised forecasts. A number of forecasters are expecting some move then or in December.

The surprise could be if one or two people did vote for further easing. MPC external member Michael Saunders recently said it was “quite likely” that additional stimulus would be needed. He could vote for action at this meeting. That would give us an idea of what form the additional easing could take – a cut in Bank Rate, further QE, or both. It might also indicate whether a consensus is likely by November or whether it’ll probably take till December. We should also watch for their discussion of growth prospects and of course what they have to say about Brexit.

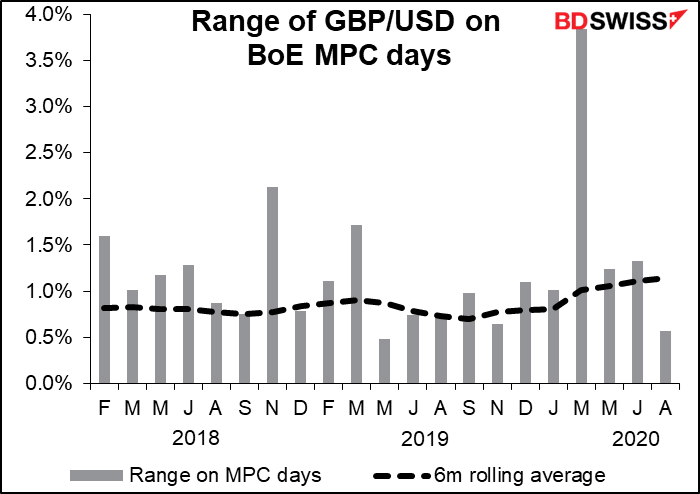

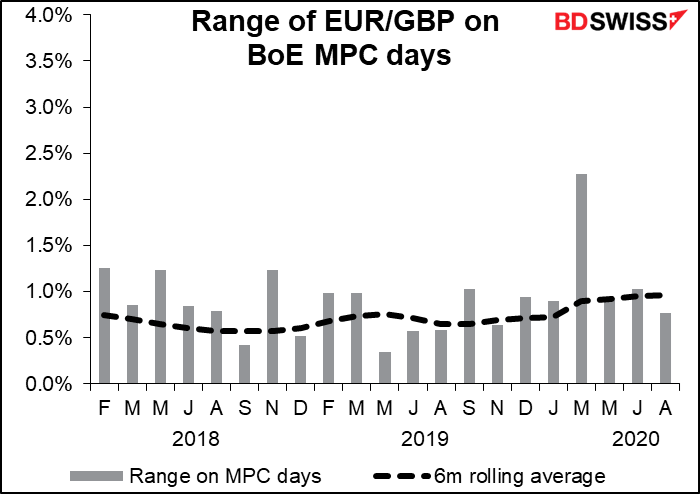

There’s no doubt – if you’re interested in taking a position in GBP ahead of the meeting, you’re likely to get more volatility in GB/USD than in EUR/GBP.

The other meeting of the day is the OPEC+ Joint Ministerial Monitoring Committee. They’ll no doubt be discussing members’ compliance with the OPEC+ production quotas as there are signs of some exporters cheating on their quotas. Several OPEC producers have cut their prices recently and on Monday, the OPEC monthly bulletin lowered their forecast for oil demand this year and next. In particular, they cut their forecast for their own crude by 700,000 barrels a day (b/d) this year and 1.1mn b/d next year, because of higher supply from non-OPEC crude and lower global demand.

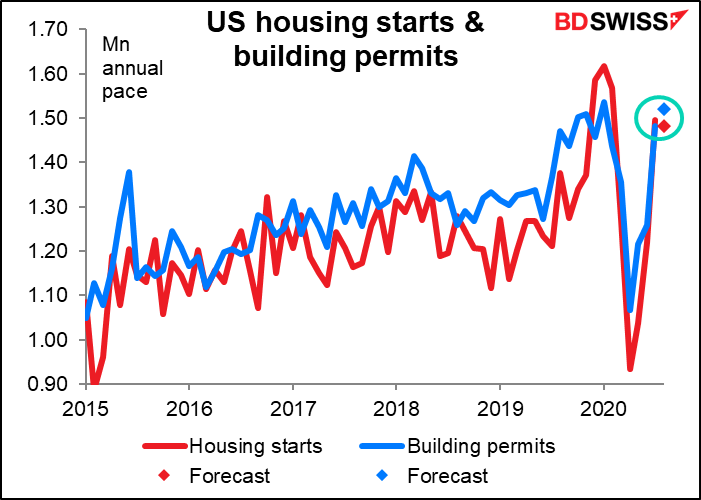

US housing starts and building permits are forecast to move in different directions – starts are forecast to decline modestly (-0.9%), perhaps because the fires on the West Coast are interfering with building there. Permits on the other hand are expected to continue their upward trend (+2.5%) in response to pent-up demand from earlier in the year plus the new migration out of the cities into the ‘burbs. That’s probably a more accurate picture of the state of the US housing market now.

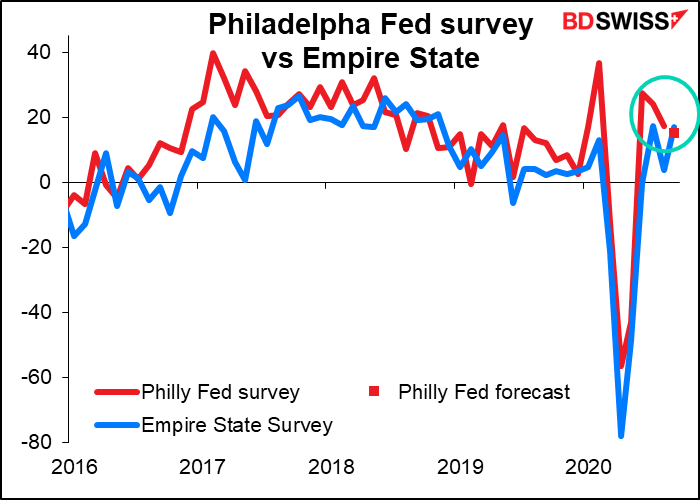

The Philadelphia Fed business outlook is supposed to be just a bit lower. This compares with Tuesday’s Empire State manufacturing index, which was expected to be a bit higher (6.9 vs 3.7 previously) but turned out to be a lot higher (17.0). An upside surprise here too might help the dollar.

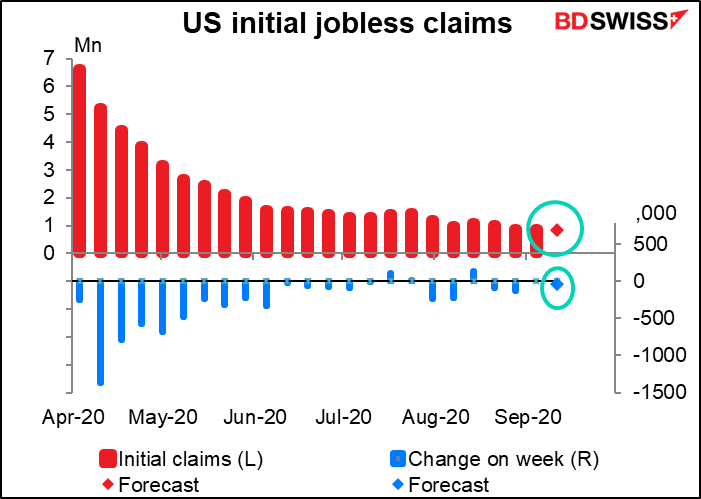

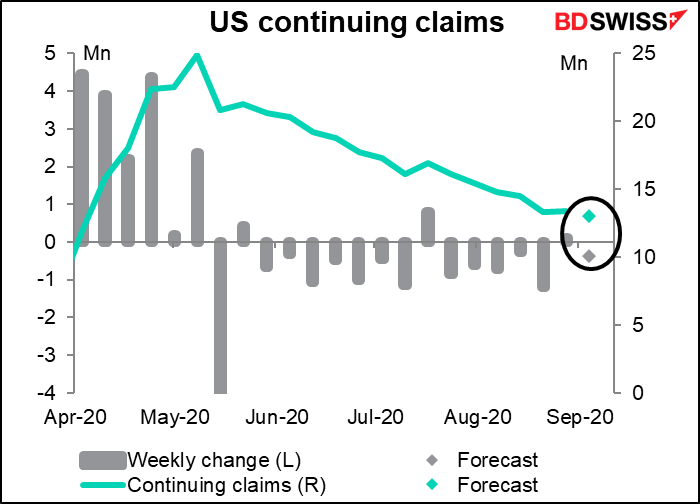

Next is our new weekly ritual: the US jobless claims. They’re expected to show a tiny decline in both initial and continuing claims, which I suppose is better than a tiny rise, but it’s still pitiful. The August payroll report showed an encouraging rise in jobs, but last week’s jobless claims showed signs of stalling, with initial claims unchanged on the week and continuing claims increasing. California was responsible for a large part of those increases, probably due to the fires.

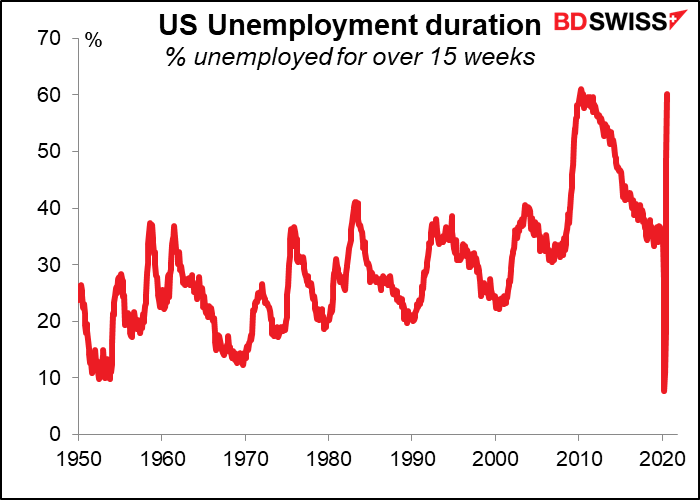

One worrisome aspect of the unemployment problem in the US is the duration of unemployment. People are finding themselves unemployed for longer and longer –

in August, 60.1% of the unemployed people had been unemployed for longer than 15 weeks, which approaches the record for this dismal metric (61.1% in April 2010). This is particularly worrisome as more and more workers roll off the state unemployment programs (which are only good for 26 weeks in most states) and onto federal programs, which are not included in the “continuing claims” data.

(The big dip in this data in early 2020 was in April, when all of a sudden millions of people suddenly lost their jobs.)

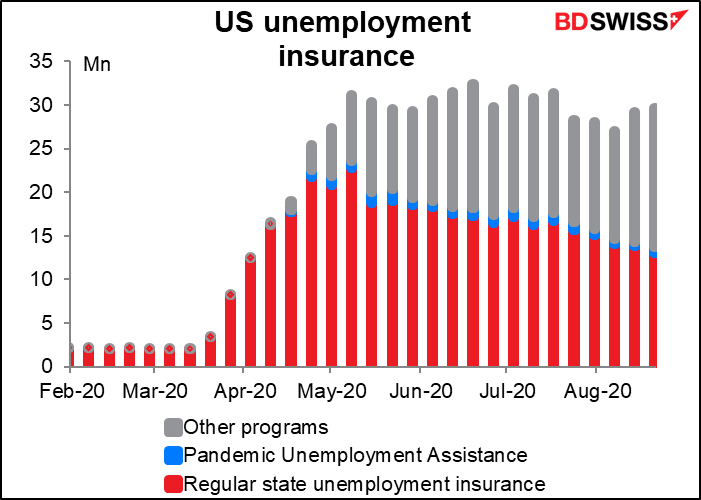

We therefore have to watch the data the total number of workers applying for unemployment benefits from all programs, which is going in the wrong direction – it was up 380k to 29.6mn people in the latest week (21 August) and up 2.2mn the week before. This is the real picture of unemployment in the US.

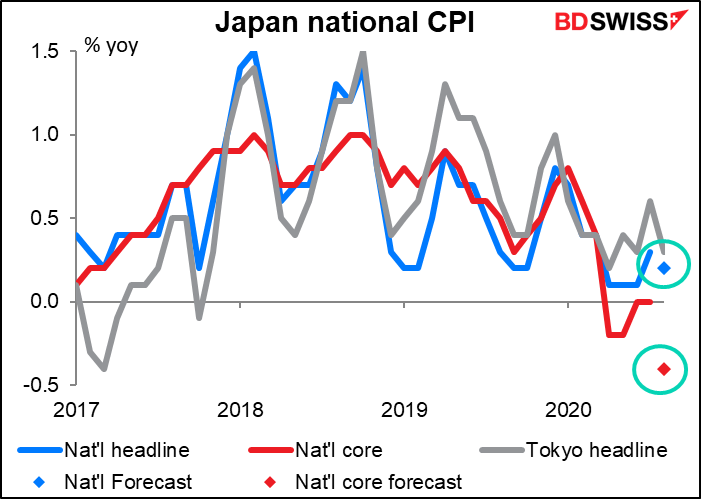

Overnight we get the King of Useless Statistics, the Japan national consumer price index (CPI). The headline rate of inflation is expected to be down a little while core inflation is expected to be down a lot (Japan’s core inflation only excludes fresh foods, not energy – the CPI excluding fresh foods and energy is called “core-core” inflation and no one watches it, for reasons beyond me.) The main reason for the sudden drop is the government’s “Go To Travel Campaign.” The program, which began in late July, subsidizes some of the costs of domestic travel. In any case, Japan’s experience should be a warning to all the other central banks that think low interest rates and quantitative easing are going to get inflation back up to their 2% target.

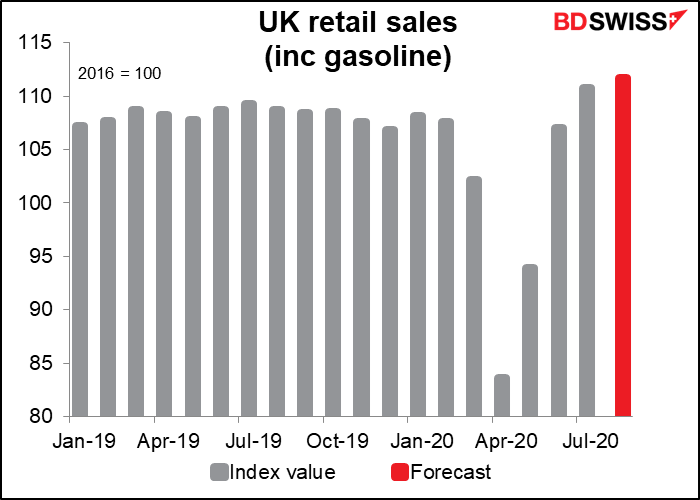

Then just as people in the UK are trying to remember whether to pour the milk in first, then the tea, or is it the tea first, then the milk, we get UK retail sales. Retail sales was the first key UK data series to regain its pre-pandemic level back in June. However, it looks like spending is slowing down as consumer confidence wanes and unemployment rises.