Rates as of 05:00 GMT

Market Recap

A relatively quiet day for data and an absence of headlines about the coronavirus led to a “risk on” day during the European and US days. However, this morning in Asia, investors got a shock after Hubei Province, the epicenter of the virus, revised its way of calculating the numbers affected. The inclusion of people who are “clinically diagnosed” increased the number of confirmed cases by 14,890 just as people were beginning to think that the epidemic had peaked on 4 February, when the number of new cases every day started to decline. The increase sent markets into a tailspin, although some people argued that it’s better now that officials are being honest and transparent rather than trying to hide the severity of the outbreak.

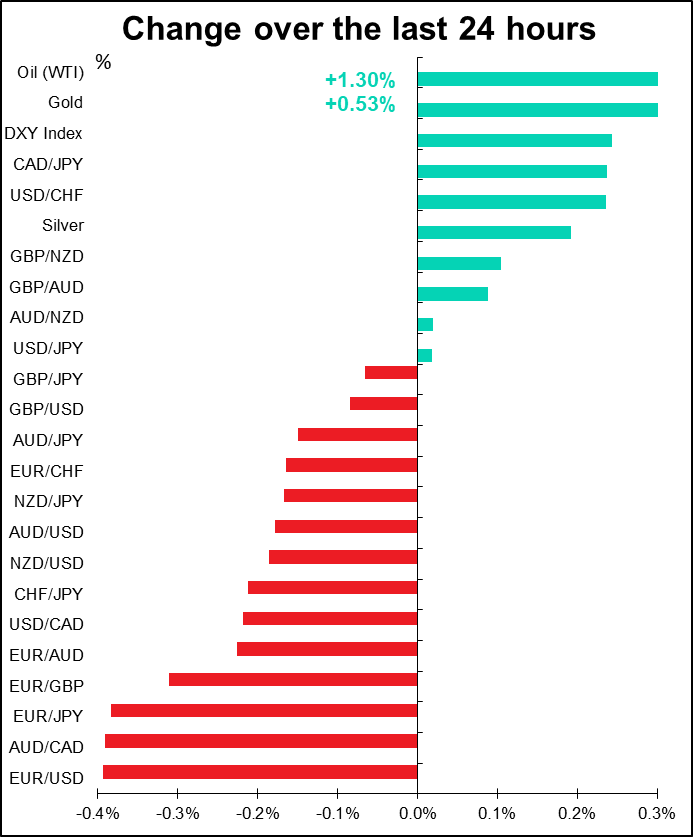

The news from China makes it seem likely that we could see a reversal of Wednesday’s trends today. The “risk on” move that pushed oil prices up 1.3% and helped make CAD the best-performing currency overnight is starting to reverse. The graph shows how Brent oil (white line) is following USD/CNH (red line, reversed) this morning.

By the way, if you’re looking to keep track of the virus, Bloomberg now has a page dedicated to it on their website. There may be a limit to how many times a month you may access this without paying, however.

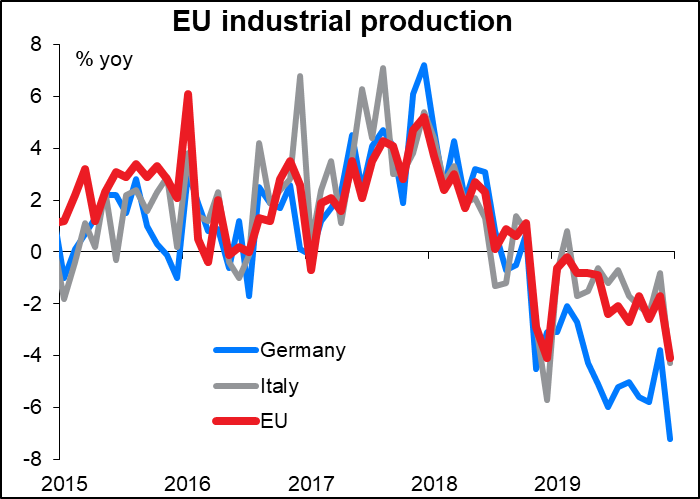

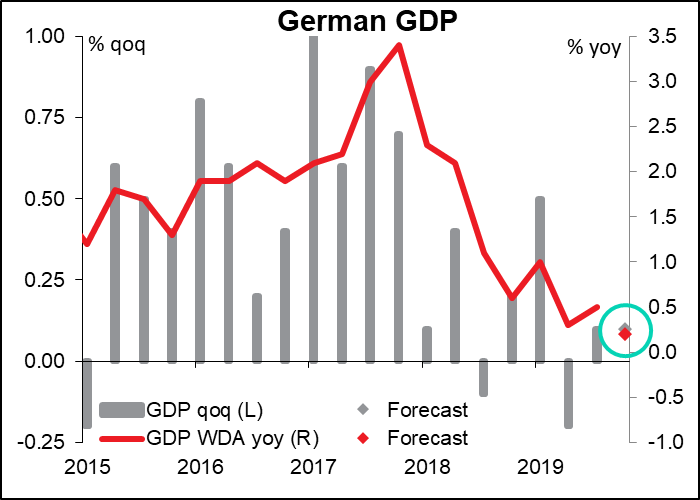

EUR on the other hand was the worst-performing currency, for several reasons. One, there’s starting to be a lot of concern about the strength of the Eurozone economy after disappointing industrial production (IP) figures from the major countries, notably Germany and Italy. Yesterday’s EU-wide IP data was much worse than expected, with the yoy rate of decline accelerating to o-4.1% yoy from -1.7% (-2.5% expected).

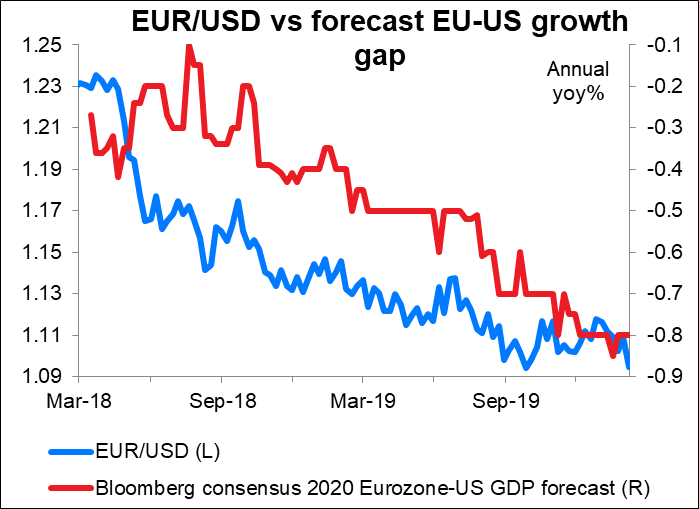

The market forecast is that Q4 2019 represented the trough of activity and the EU economy should rebound starting in 2020, but if momentum was this poor at the end of last year and now we’re confronting the crisis in China, people are starting to think that maybe the economic forecasts for Europe are a bit optimistic. And if EU growth gets revised down relative to US growth,then it’s likely EUR will fall further relative to USD.

The political problems in Germany may also be weighing on the currency. German Chancellor Merkel’s heir apparent, Annegret Kramp-Karrenbauer, resigned on Monday as the chair of Merkel’s CDU party, leaving the leadership of the ruling coalition in Europe’s leading economy in disarray. The problem is not only who will succeed Merkel, but also whether the ruling coalition will even remain in power after the next federal elections, which are scheduled for September 2021 (but could be called earlier).

Furthermore, the euro’s use as a funding currency is depressing its value as more and more US companies raise money in euros and move it back to the US.

I think these problems are likely to continue to weigh on the euro and the single currency may decline further over the next few months.

One indication of the euro’s problems: EUR/CHF has tended to remain weak even on days when risk sentiment is recovering as momentum traders have jumped onto this trade. This has increased the correlation between EUR/USD and EUR/CHF.

Today’s market

Did you miss ECB Chief Economist Lane’s speech yesterday? Don’t worry – you’ll have not one but two chances today to catch up with what he has to say.

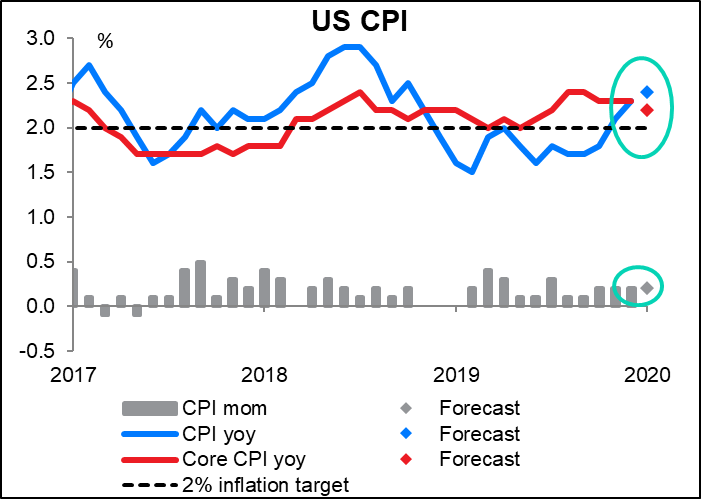

The important indicators don’t start until Uncle Sam wakes up and the US consumer price index (CPI) comes out. This isn’t the Fed’s preferred inflation gauge – that’s the personal consumption expenditure (PCE) deflator – but the market pays close attention to it anyway, because to most people this is the definition of inflation.

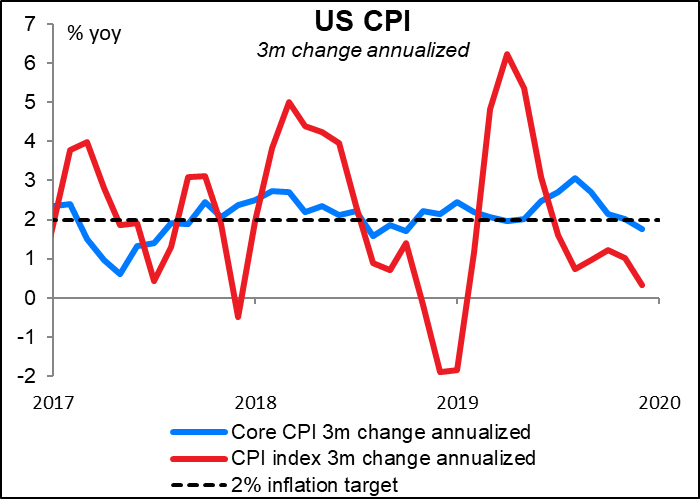

The picture looks very different just from the recent data, however. If we take the three-month change of these two indices and annualize it, we see that the trend in US inflation is distinctly downwards. Core inflation calculated this way is about at the target, but headline inflation is almost nothing – and is set to go even lower in the coming few months as falling oil prices feed through the economy.

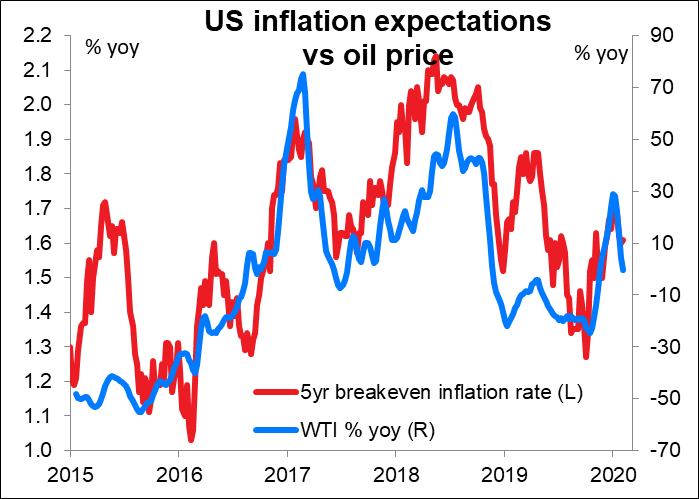

Furthermore, inflation expectations in the US basically seem to be a function of the oil price. Expecations now are pretty much in line with the Fed’s target. However, with oil prices falling, the Fed may be concerned not just about inflation turning down, but also about the possibility of inflation expectations turning down too.

Now we come to what may be the closest we get to a train wreck in finance: the Senate Banking Committee hearing into the nomination of Christopher Waller and Judy Shelton to be governors on the Federal Reserve Board.

Waller is quite a standard pick for the Fed Board. Apparently Trump wanted St. Louis Fed President Bullard, but Bullard – one of the most dovish people on the FOMC – declined. So instead Trump picked Waller, who was Bullard’s mentor while the latter was studying for his PhD in economist at Indiana University and is currently the Director of Research at the St. Louis Fed. He too is quite dovish, but he’s also a strong proponent of central bank independence.

Shelton on the other hand…as my grandmother would say, oy vey iz mir. I won’t dwell on the fact that she doesn’t have an advanced degree in economics – neither does Fed Chair Powell. But really… She’s best known for her support for putting the world back on the gold standard.

She’s a bizarre candidate for the central bank. According to Wikipedia, she’s said that she’s “highly skeptical” of the Fed’s “nebulous” dual mandate of maximum employment and price stability. She’s written that a “fundamental question” of economics is “why do we need a central bank?”

During the Obama years she described low interest rates as “an assault on democratic capitalism,” but now she urges the Fed to lower rates to support the Trump agenda. She’s advocated another Bretton Woods conference to reshape the international monetary system – to be held at Trump’’s Mar-a-Lago resort, of course. At least she’s consistent in one way — she’s said that she saw “no reference to independence” in the Fed’s authorizing legislation.

What chance does she have to get approved? Ordinarily, I would be talking about snowflakes and hot places. Trump’s last four nominees have failed to get approval, including such conventional picks as Prof. Marvin Goodfriend and Nellie Liang, a former Fed researcher and Director of the Fed’s Office of Financial Stability.

The big fear is that Trump may be angling to get Shelton in place to take over from Powell when his term ends in 2022 – assuming of course that Trump is still in a position to make appointments then.

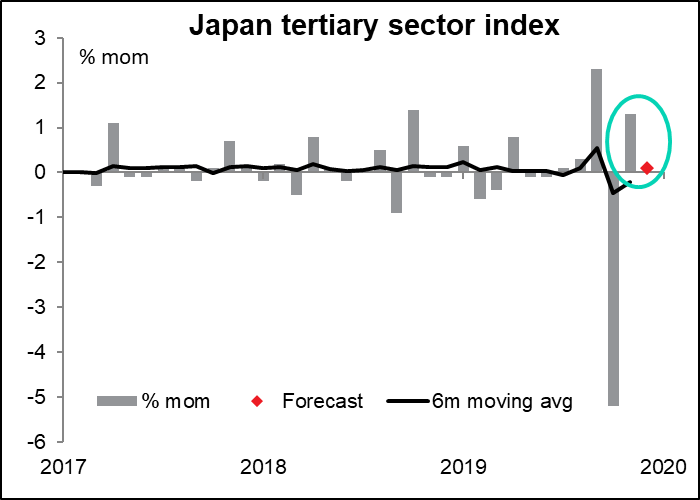

In Japan, the tertiary sector index comes out. According to Bloomberg this is closely watched, but I don’t think it’s closely watched by FX traders. If it is, I bet they’re bored, because outside from the surge in September and the plunge in October – thanks to the hike in the consumption tax in October – it seems to be trending pretty steadily at around +0.1% mom, ±0.1%. This month is forecast to be right in line with the average at unchanged.

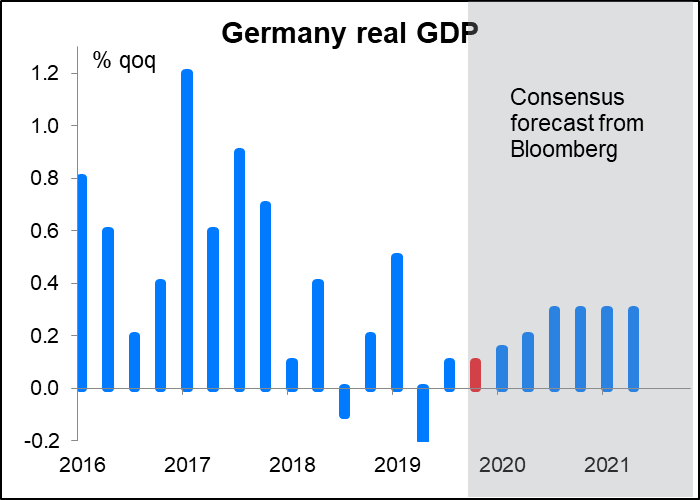

Finally, as Europe shakes the sleep out of its eyes, we get the preliminary estimate of Germany’s 4Q GDP. This is not likely to be a surprise, as they’ve already announced GDP for 2019 as a whole, which allows the mathematically talented analyst community to back out what Q4 alone was.

You may be getting tired of seeing this same graph over and over, but it seems to be the general view of the world economy among analysts now – that Q4 2019 was the trough and we’ll have a gradual recovery during 2020. Although in the case of Germany, it looks like the recovery is not expected to be particularly robust. The consensus forecast is for growth to recover to +0.3% QoQ during the second half of the year, which would be OK but nothing special.

The second estimate of EU-wide GDP comes out a few hours later, but this is normally of interest only with regards to the details – the overall figure is rarely revised, and if it is, it’s only ±0.1 percentage point, which isn’t that important.